[ad_1]

The time interval personal finance ratios may give you flashbacks to math class, learning quite a few formulation, equations, and ratios. Once more then, if school college students appeared like they’d been zoning out, your teacher may have instructed you “pay attention, it will in all probability be useful to you later.” Properly, this time, you don’t should attend—a great deal of the equations beneath will in all probability be useful to you correct now!

Let’s examine further about what ratios are and fourteen of the very best money ratios it’s best to use as we communicate!

What’s a personal finance ratio?

In mathematical phrases, a ratio is mainly a method to look at two numbers. Since finance is all about numbers, which will become helpful in some methods significantly when making financial calculations!

It’s best to make the most of ratios to take care of observe of many various options of your financial situation—from cash stream to monetary financial savings to concepts for retirement planning and additional.

A typical ratio is expressed as a divisible amount, nevertheless among the many ones beneath use multiplication or subtractions instead.

Lastly, merely think about it as a method to look at your money and the best way you utilize it. Conserving a report of your money ratios could illuminate how these numbers change over time.

14 of primarily probably the most useful personal finance ratios

The best technique to make clear the ratios is just to start displaying you examples! So beneath, we’ll make clear recommendations on how you can use every and why they’re typically helpful to your journey.

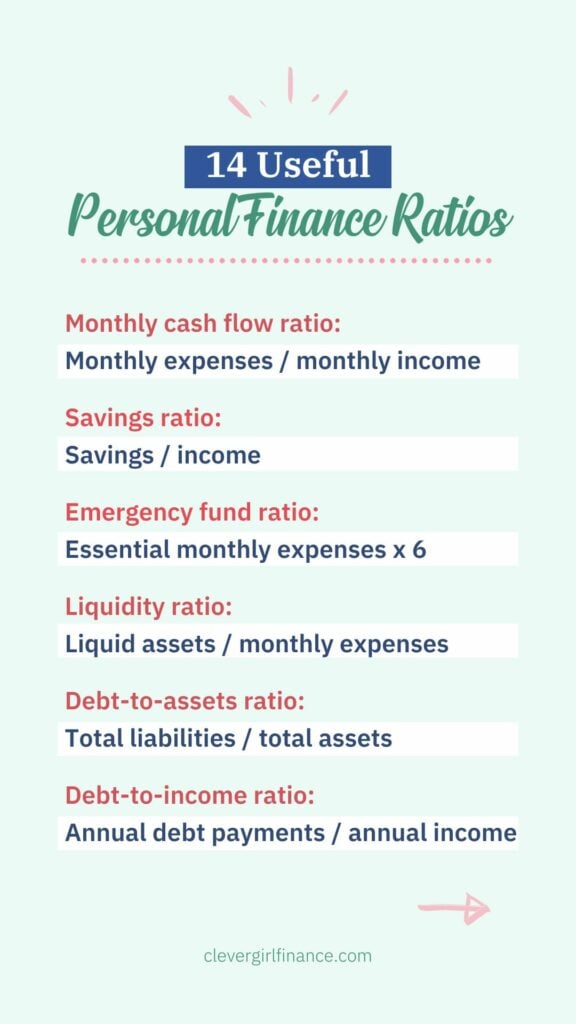

1. Month-to-month cash stream ratio

Month-to-month payments divided by month-to-month income

The month-to-month cash stream elements helps you understand what share of your income is dedicated to your month-to-month payments. Take into accounts the cash stream ratio as how loads cash flows in vs flowing out.

Start by together with up your entire frequent income from jobs, facet gigs, funding income, and so forth. It’s best to make the most of a gross decide or your exact take-home pay (aka net income) after taxes.

Then, create or search recommendation out of your spending journal or a value vary template or instrument to see how loads you spend every month. Don’t embrace monetary financial savings or investments in your spending calculations (that has its private personal finance ratio)! All of the issues else is trustworthy recreation: necessities, car funds, satisfying money, presents, month-to-month cash owed, and so forth.

Do you have to spend spherical $2,000 month-to-month and make $2,500, your cash stream ratio could be $2,000 / $2,500 = 80%. It tells you that 80% of your income is spent on payments.

2. Monetary financial savings ratio

Month-to-month monetary financial savings divided by month-to-month income

That’s primarily the flip facet of the one above. As an alternative of telling you the best way loads you’re spending month-to-month, it tells you your monetary financial savings value.

Embody all kinds of monetary financial savings proper right here. Whether or not or not you’re putting money in a monetary financial savings account, your group’s 401(okay), your personal IRA, an funding account, and even keeping apart bodily cash, it qualifies.

Using the an identical month-to-month numbers as above, let’s say you’re putting the rest of your money ($500) in route of economic financial savings and investments.

Your month-to-month monetary financial savings ratio could be $500 / $2,500 = 20% monetary financial savings value. You’ll be able to even do the an identical to look out your annual monetary financial savings ratio. Meaning, you’ll decide when you want to save further to dwell greater or if the amount you save is sensible.

3. Emergency fund ratio

Essential month-to-month payments x 6

An emergency fund exists to protect you inside the event of unusual payments or job loss. It’s money you want to keep merely accessible so it’s best to use it as rapidly as needed.

As a full-time freelancer, I’ve had months the place I’ve a ton of purchasers and initiatives, along with months the place enterprise is barely slower. My emergency fund offers me peace of ideas that I gained’t be in a dire situation if my work schedule changes.

Given that widespread information is to save lots of a number of 3-6 months of payments in your emergency fund, this ratio shows that. Merely multiply your essential month-to-month payments by 6 to provide you your objective for a completely stocked emergency fund.

After I say “essential,” I indicate chances are you’ll be slicing out just a few of your “satisfying” budgets for this one. Merely embrace the problems you’ll’t dwell with out (housing, utilities, meals, medical insurance coverage, and so forth).

Our occasion particular person would possibly often spend $2,000 a month, nevertheless let’s say that they’ll pare down their essential payments to $1,500. $1,500 * 6 = $9000 could be the objective for his or her emergency fund.

Keep this money in an interest-bearing account—ideally, a high-yield monetary financial savings account. Meaning, it ought to keep accessible everytime you need it, nevertheless the curiosity will help you develop your money whereas it’s there!

4. Liquidity ratio

Liquid property divided by month-to-month payments

The liquidity ratio is among the many personal finance ratios fastidiously tied to your emergency fund since they every revolve throughout the idea of liquidity. Put merely, liquid property search recommendation from (A) cash or (B) totally different financial property you’ll quickly convert into cash.

Money in a checking, monetary financial savings, or money market account is extraordinarily liquid. In case you’ve gotten monetary financial savings bonds you’ll cash in any time, they’re liquid.

In case you’ve gotten shares, bonds, index funds, and totally different “cash equivalents” or totally different extraordinarily liquid investments that you might merely promote within the market, they’d qualify as liquid, too. (However, their value fluctuates further, so it’s not a safe amount).

In actual fact, you’ll’t merely promote your individual house on a whim for quick cash, so that’s an excellent occasion of a non-liquid asset. Money saved in retirement accounts could be illiquid since withdrawals are subject to loads of pointers and take time.

After getting these figures, working the liquidity ratio elements will reveal what variety of months your liquid net value would possibly help you. So for anyone with $20,000 in liquid property who spends $2,000 a month, it’s $20,000 / $2,000 = 10 months of coated payments.

5. Debt-to-assets ratio

Full liabilities divided by complete property

Now we’re transferring into some doubtlessly a lot much less satisfying territory: just a few debt ratios. Don’t be scared in case your numbers are elevated than you’d like at first. It’s all part of your debt low cost journey!

Do you have to don’t know the place you’re starting from, you’ll merely be stumbling spherical at nighttime, hoping your debt will in all probability be gone sometime.

You may also hear the debt-to-assets ratio known as a solvency ratio. (Often, “solvency ratio” is a time interval used for firms further often than folks.) It’s a method to see whether or not or not you’ll repay your cash owed by selling your property.

Start by together with up your faculty loans, any shopper debt like financial institution playing cards, personal loans, car loans, and irrespective of totally different form of debt you carry.

Then, calculate the price of your key property, along with all monetary financial savings and funding accounts, paid-off autos, and personal valuables.

In case you’ve gotten $10,000 in complete liabilities and $40,000 in complete property, you have gotten $10k / $40k = 25% as loads debt as property.

Is a house counted as an asset or obligation?

What about your personal house? Is a house an asset or a obligation? It’s every! Besides your mortgage is paid off, you have gotten equity in your individual house and debt on the same time.

House owners can choose whether or not or not or to not add their remaining mortgage stability as debt and residential equity as an asset on this ratio.

Keep in mind that since mortgages are the most important loans most people might have of their lives, along with it might presumably make your ratio seem skewed. Do you have to like, you’ll run the numbers with and with out the home factored in to see the excellence.

6. Debt-to-income ratio

Annual debt funds divided by annual income

That is among the many personal finance ratios which will help you identify how numerous your income is being funneled in direction of your cash owed yearly.

To start out out your equation, take a look on the cash owed you gathered above. Nonetheless this time, add up your yearly funds in route of each of them.

One exception is that for individuals who’re a home proprietor, it’s best to exclude mortgage debt from this equation—that’s a surefire method to kill your ratio! (Plus, housing funds fall further into common payments than debt payoff.)

Subsequent, you’ll divide your annual cash owed by your annual income. Often, people use their gross income pretty than net income for this calculation. Embody any income from facet gigs and numerous sources as successfully.

As your cash owed shrink, the outcomes of this ratio will, too! Nonetheless for individuals who’re together with new cash owed or paying points off too slowly, compound curiosity may enhance your debt funds and, subsequently, this ratio.

Someone making $15,000 in annual debt funds whereas incomes $50,000 a 12 months is paying $15k / $50k = 30% of their income to their debtors.

For companies, an an identical ratio known as the “debt servicing ratio” helps lenders assess a enterprise’s debt compensation ability.

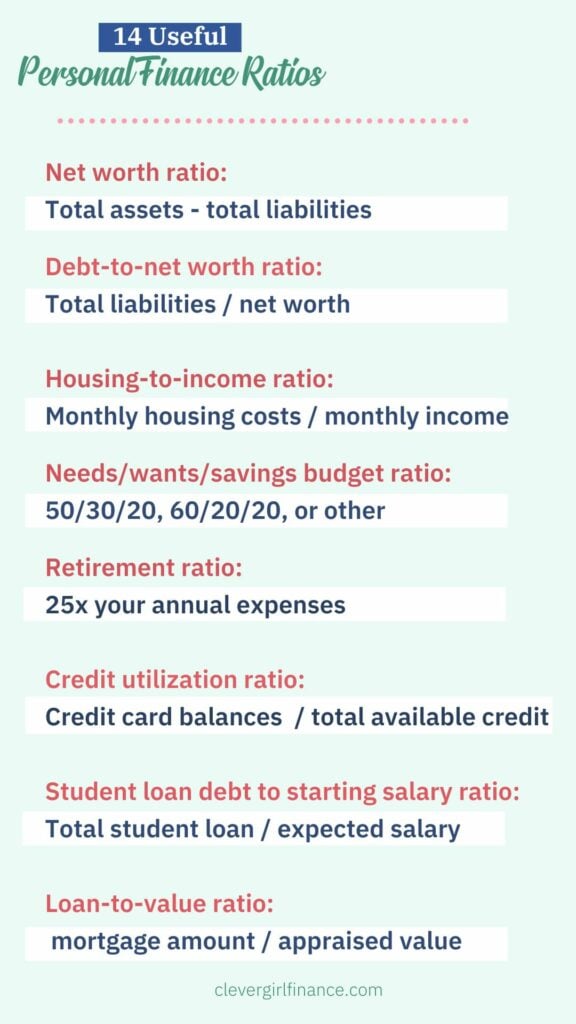

7. Web value ratio

Full property minus complete liabilities

The net value ratio goes to be fast and sweet! Seize the an identical numbers you utilized in #5, nevertheless instead of dividing, we’ll merely subtract.

Property minus liabilities help you calculate your net value! It’s motivating and fulfilling to look at this amount develop over time.

$40,000 property – $10,000 liabilities = $30,000 net value.

8. Debt to net value ratio

Full liabilities divided by net value

That’s just like the debt-to-assets ratio.

However, you aren’t merely evaluating complete debt to complete asset value with this one. As an alternative, you’re evaluating your debt to the net value decide from #7—the place debt has already been subtracted out of your asset value.

The ratio is meant that can assist you determine how loads debt you’ve taken on relative to your net value.

In case your ratio is over 100%, you would possibly actually really feel over-leveraged and battle with funds. The lower the top consequence, the additional comfortable you’ll actually really feel alongside along with your debt ranges.

$10,000 liabilities / $30,000 net value = 33% debt to net value ratio.

9. Housing-to-income ratio

Month-to-month housing costs divided by month-to-month income

You’ve possibly heard some advice for spending a certain share of your income on housing. Beforehand, the rule of thumb amount was 30%. Now, there’s a barely further detailed model known as the 28/36 rule.

The first half (28) means it’s essential to goal to spend no more than 28% of your income in your complete house price, along with taxes and insurance coverage protection.

The second half (36) offers your mortgage price to your entire totally different debt funds and recommends that this complete not exceed 36% of your income. It’s efficiently the an identical issue as your debt-to-income ratio from #6 (nevertheless a mortgage-inclusive mannequin).

The 28/36 rule is a implies that will assist you weigh whether or not or not your personal house purchase would put you in an extreme quantity of debt.

For instance, if a attainable dwelling purchase would bump you too far over the 36% debt-to-income decide, you may want to take a look at cheaper properties. In some other case, you run the prospect of turning into house poor!

Do you have to’re spending $1,000 a month on housing whereas making $3,500, you’re spending $1k / $3.5k = practically 28% on housing.

10. Desires/wishes/monetary financial savings value vary ratio

50/30/20, 60/20/20, or totally different

Want a personal finance ratio that gives you a quick info on dividing your payments? There are a variety of strategies to do this.

Usually, the very best methods comprise breaking down your payments into needs, wishes, and monetary financial savings. Desires are each factor you’ll’t dwell with out, wishes are the nice-to-haves, and monetary financial savings are what you place aside to your future.

The 50/30/20 rule

One widespread value vary ratio generally known as the 50-30-20 rule. On this elements, 50% of your income goes to necessities, 30% is reserved for discretionary income, and 20% will get saved.

Let’s see how this may work for anyone who makes $3,000 a month. The 50/30/20 ratio would indicate $1,500 goes to needs, $900 to wishes, and $600 to monetary financial savings/investments.

Completely different percentages

All of these numbers could possibly be tweaked relying in your situation.

So for individuals who’re spending 60% of your income on necessities, you may want to goal for further of a 60 20 20 breakdown or even the 70-20-10 value vary.

11. Retirement ratio

25x your annual payments

Ever find yourself asking, “Can I retire however?” If you stop working, you want to be assured that your monetary financial savings and investments may have the flexibility to proceed funding your life.

It’s a tried-and-true methodology for understanding what you need in retirement. It’s moreover based totally on one factor known as the 4% rule, which refers back to the idea {that a} retiree can safely withdraw 4% of their monetary financial savings yearly with little menace of understanding.

Calculating your retirement payments

Take a look at your current annual payments and check out to find out within the occasion that they’ll be elevated or lower in retirement. Possibly you’ll have a paid-off house by then and eradicate lease/mortgage payments.

On the flip facet, you may want to try full time touring or have additional for medical care. It on no account hurts to pad the numbers, nevertheless the 25x payments elements is an effective place to start.

Someone who spends $50,000 a 12 months would ideally want $50,000 * 25 = $1.25 million to retire confidently.

12. Credit score rating utilization ratio

Sum of financial institution card balances divided by complete obtainable credit score rating

Your financial institution card utilization ratio helps current how efficiently you deal with your obtainable credit score rating. Extreme utilization would possibly signify that you have an unhealthy reliance on debt.

Utilization could be an unlimited think about determining your FICO credit score rating score, so it’s value taking note of for individuals who’re trying to reinforce your credit score rating. Understanding and managing this ratio can positively impression your creditworthiness and financial well-being.

Figuring out your credit score rating utilization

To calculate it, take the current sum of your revolving credit score rating account balances and divide it by the entire credit score rating limits all through your entire accounts.

A lower credit score rating utilization value helps your credit score rating score. Avoid going over a 30% credit score rating utilization ratio—holding it at or beneath the ten% range is true. Give consideration to paying off wonderful cash owed and limiting the balances you carry from one month to the next.

Take into consideration a state of affairs the place your financial institution card balances amount to $2,000, and your complete credit score rating limits all through all taking part in playing cards are $10,000. The credit score rating utilization ratio could be $2k / $10k = 20%. Because of this you simply’re using 20% of your obtainable credit score rating.

The benefit of utilization is that it primarily changes every month. Even when you’ve gotten a extreme ratio for one month, you’ll pay down your balances and return to a low utilization in a short time.

13. Pupil mortgage debt to starting wage ratio

Full amount of pupil mortgage, divided by anticipated starting wage

Faculty is notoriously expensive. And besides you know how to get a full journey scholarship or have a faculty fund, it could be laborious to stare these pupil mortgage offers and charges of curiosity inside the face and ask your self, is it value it?

The debt-to-salary ratio offers a straightforward info for varsity school college students and their households to help reply this question. Will your diploma be nicely definitely worth the debt in the long term?

This elements helps you identify the utmost mortgage amount to borrow for a specific diploma program.

How do I inform if my faculty diploma will in all probability be value it?

Since you’ll’t predict the long term, it’s unattainable to calculate the exact ROI (return on funding) for a faculty diploma. Nonetheless you’ll take a look on the job market in your objective topic and determine what starting income you’ll depend on after graduation. Internet sites like wage.com would possibly assist with this evaluation.

Your outcomes may even help you propose a smart debt compensation schedule to your faculty loans. As a rule of thumb, school college students ought to limit their debt-to-starting-salary ratio to decrease than 100% to repay the loans over roughly a 10-year interval. (In actual fact, charges of curiosity can impact the exact timeline.)

So, let’s say you take out $30,000 in loans, and your anticipated starting income is $50,000. The debt to starting wage ratio could be $30,000 / $50,000 = 60%. The tip consequence signifies that your debt could be 60% of your anticipated starting wage, which is relatively conservative and low-cost.

Then once more, borrowing $60,000 for a degree that leads to a median starting wage of $30,000 would not make as loads financial sense. Which may put the ratio finish consequence at 200%—double the advisable amount.

It would not matter what your diploma costs, enroll in our free pupil loans 101 course bundle to ensure you clearly understand how they work.

14. Mortgage-to-value ratio

Remaining mortgage amount on a property, divided by its appraised value

The loan-to-value (LTV) money ratio is a vital metric inside the realm of precise property financing. Lenders reference this ratio as a part of the mortgage approval course of. Moreover they ponder it for refinancing and residential equity line of credit score rating (HELOC) capabilities. A low LTV is good because you owe a lot much less on the mortgage.

Whether or not or not you’re a gift home-owner or a potential first time dwelling purchaser, this personal finance ratio will in all probability be associated to you.

How the LTV ratio works for model new dwelling shoppers

Do you have to’re searching for a home, your preliminary LTV will depend on the dimensions of your individual house down price. Let’s say you place 20% down on a house valued at $200,000, so your down price is $40,000 and your mortgage is $160,000.

That makes your LTV ratio equation $160,000 / $200,000 = 80%.

Do you have to solely put 10% down, you’ll be left with an LTV of 90%. Higher LTVs on new dwelling purchases can embrace further costs, like elevated mortgage charges of curiosity and private mortgage insurance coverage protection (PMI).

The larger your down price is, the smaller your LTV will in all probability be, and vice versa. Saving up not lower than a 20% down price will get you primarily probably the most favorable phrases.

How the LTV ratio works for homeowners

For current homeowners, the LTV represents how loads equity has constructed up in your own home, i.e. how numerous the mortgaged property you private. This decide moreover determines whether or not or not you’ll refinance at a lower price of curiosity or entry a home equity line of credit score rating.

Your LTV will decrease as you pay your mortgage, nevertheless it might presumably moreover change in case your appraised property value changes.

In some circumstances, LTV can enhance if a property’s market value drops. It should in all probability happen if there’s property damage (e.g. from flooding) or a recession hits. Nonetheless it’s quite extra widespread to your LTV to decrease as your precise property value grows, which is a helpful change.

Let’s say you bought our occasion dwelling when it was valued at $200,000. After 5 years, you proceed to owe $125,000, nevertheless your property value has appreciated to $250,000. That new value is the decide you’ll use for the ratio: $125,000 / $250,000 = 50% instead of $125,000 / $200,000 = 62%. It’s like getting additional equity with out spending a dime!

Skilled tip: Take into consideration money ratios all through the context of your life

Okay, you’ve merely gone by way of a great deal of math—take a breath! Now could possibly be the time to remember these math equations are most insightful everytime you put them into context. A single ratio isn’t going to provide an entire view of your financial nicely being.

It is best to on no account actually really feel harmful if just a few of your ratio outcomes are above or beneath the very best numbers. You don’t have to dwell and die by money ratios! They’re solely a info, and there’s always room for exceptions and adaptableness based totally in your distinctive situation.

Maybe your required faculty diploma doesn’t embrace an incredible starting wage…however it’s a topic you’d love working in, with good future progress alternate options. Don’t rule it out because of a math equation.

Take into consideration all of them all through the context of your personal core values, needs, and targets to make them be simply best for you.

Why are personal finance ratios needed for you?

These ratios are good strategies to distill tried-and-true financial information into straightforward formulation that anyone can use.

In case you want to know whether or not or not your monetary financial savings are on observe—there’s a ratio for that. Curious for individuals who’re spending an extreme quantity of on housing? There’s a ratio for that.

Realizing your financial numbers would possibly assist you improve your life

Furthermore, holding a report of these numbers lets you replicate on the place you bought right here from. As you examine new frugal life hacks, you’ll pare down your payments and improve your cash stream ratio.

As your income grows and likewise you repay debt, these debt ratios shrink in entrance of your eyes whereas your net value swells.

They’re some satisfying little equations that give you one different method to look at your funds and set new targets.

What are essential ratios for money?

Finance is a extraordinarily individualized journey, so the importance of explicit ratios can differ based totally on explicit individual circumstances and financial targets. Nonetheless sometimes, there are only a few ratios that everyone should be taking note of.

The emergency fund ratio is one amongst my excessive ideas for the beginning of your financial journey. Life can throw curveballs at anyone, anytime.

Having not lower than six months of payments squirreled away helps give you a runway to find out points out for individuals who get laid off, should pay for a shock dwelling or car restore, and so forth.

I’ll moreover highlight the monetary financial savings ratio, which contains standard monetary financial savings and investments. Monetary financial savings are primarily your key to the long term. They put your entire targets in attain, whether or not or not it’s searching for a house, paying off your loans, or early retirement.

What’s an efficient debt to net value ratio?

An awesome debt to net value ratio strikes a healthful stability between leveraging debt for wealth-building and avoiding excessive indebtedness.

You may assume it’s best to try for no debt.

However, whereas which can be a worthy goal for some people, it isn’t always the case. In some circumstances, debt is often a instrument that can assist you greater your financial nicely being.

It ties into the concept of kinds of debt, like good debt vs. harmful debt.

As an illustration, pupil mortgage debt or enterprise debt would possibly assist you make more cash all by your lifetime. Nonetheless financial institution card debt will eat your income with its high-interest costs.

You can give it some thought in the case of these ranges:

- Most safe range: A ratio beneath 50% is generally considered healthful—indicating that your net value will not be lower than twice your complete debt.

- Common range: Ratios between 50-100% can nonetheless be manageable, counting on the situation. Think about the types of debt you have gotten, its operate, and whether or not or not it contributes to your basic financial well-being.

- Cautionary ranges: Ratios exceeding 100% level out that your complete debt surpasses your net value. It alerts the subsequent diploma of financial menace, so proceed fastidiously and assure you have gotten a robust debt compensation method.

Articles related to organized funds and financial literacy

Do you have to’ve added these ratios to your financial toolkit, you’ll love these reads!

Calculate your personal finance ratios!

Now it’s formally your flip!

With a view to start crunching the numbers, you’ll need some key objects of data in entrance of you. The precept stuff you’ll need embrace:

- Full annual income

- Full month-to-month income

- Full cash owed/liabilities

- Month-to-month payments (broken down by class)

- Full asset value

- Liquid asset value (aka cash or points you’ll quickly flip into cash)

- Credit score rating limits in your taking part in playing cards

- Precise property value (for property homeowners)

After getting these figures in entrance of you, the remaining is just plug-and-play. You can recalculate these personal finance ratios as often as you want—say, as quickly as a month, as quickly as 1 / 4, or yearly—to carry on excessive of your personal financial plan. Over time, for individuals who hold the course, you may even uncover methods to alter into wealthy!

[ad_2]

Provide hyperlink